Do you increase with debit or credit?

Whether a debit or credit means an increase or decrease in an account depends on the account type. In traditional double-entry accounting, debits are entered on the left, and credits are entered on the right, like so: Asset accounts Debit Increase, Credit Decrease. Expense accounts Debit Increase, Credit Decrease.

for an income account, you credit to increase it and debit to decrease it. for an expense account, you debit to increase it, and credit to decrease it. for an asset account, you debit to increase it and credit to decrease it. for a liability account you credit to increase it and debit to decrease it.

When cash is received, the cash account is debited. When cash is paid out, the cash account is credited. Cash, an asset, increased so it would be debited. Fixed assets would be credited because they decreased.

Nominal accounts: Expenses and losses are debited and incomes and gains are credited.

An increase in the value of assets is a debit to the account, and a decrease is a credit. On the flip side, an increase in liabilities or shareholders' equity is a credit to the account, notated as "CR," and a decrease is a debit, notated as "DR."

Before we analyse further, we should know the three renowned brilliant principles of bookkeeping: Firstly: Debit what comes in and credit what goes out. Secondly: Debit all expenses and credit all incomes and gains. Thirdly: Debit the Receiver, Credit the giver.

Debit does not always mean increase and credit does not always mean decrease. It depends upon the accounts involved.

- First: Debit what comes in, Credit what goes out.

- Second: Debit all expenses and losses, Credit all incomes and gains.

- Third: Debit the receiver, Credit the giver.

A Mathematical Understanding of Debits & Credits

Another way to understand debits and credits in business accounting is to look at them mathematically. A simple way to distinguish between the two is to know that a debit entry always adds a positive number to the ledger, and a credit entry always adds a negative number.

To record the transaction, debit your Inventory account and credit your Cash account. Because they are both asset accounts, your Inventory account increases with the debit while your Cash account decreases with a credit.

Is debit positive or negative?

A debit is an expense, or money paid out from an account, that results in the increase of an asset or a decrease in a liability or owners equity. Debit is the positive side of a balance sheet account, and the negative side of a result item.

Key Takeaways

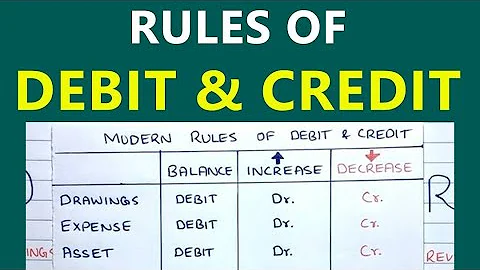

A debit is an accounting entry that creates a decrease in liabilities or an increase in assets.

What are the Golden Rules of Accounting? 1) Debit what comes in - credit what goes out. 2) Credit the giver and Debit the Receiver. 3) Credit all income and debit all expenses.

+ + Rules of Debits and Credits: Assets are increased by debits and decreased by credits. Liabilities are increased by credits and decreased by debits. Equity accounts are increased by credits and decreased by debits. Revenues are increased by credits and decreased by debits.

The Golden rule for Real and Personal Accounts: a) Debit what comes in. b) Credit the giver. c) Credit what goes Out.

- Rule 1: Debit all expenses and losses, credit all income and gain.

- Rule 2: Debit the receiver, credit the giver.

- Rule 3: Debit what comes in, credit what goes out.

Cash is flowing out of your hands in exchange for receipt of this inventory. We received inventory, so we debit the inventory account, increasing its value. Meanwhile, we paid out cash, so we'd credit the cash account.

In traditional double-entry accounting, debits are entered on the left, and credits are entered on the right, like so: Asset accounts Debit Increase, Credit Decrease. Expense accounts Debit Increase, Credit Decrease. Liability accounts Debit Decrease, Credit Increase.

Bank's Debits and Credits. When you hear your banker say, "I'll credit your checking account," it means the transaction will increase your checking account balance. Conversely, if your bank debits your account (e.g., takes a monthly service charge from your account) your checking account balance decreases.

Normal Balance of an Account

As assets and expenses increase on the debit side, their normal balance is a debit. Dividends paid to shareholders also have a normal balance that is a debit entry. Since liabilities, equity (such as common stock), and revenues increase with a credit, their “normal” balance is a credit.

How do you remember debit and credit?

The most important point to remember is the DEBIT literally means LEFT and CREDIT literally means RIGHT. Let's take a look at one more example, also from NeatNiks.

Debit Balance in Accounting

Accounts that normally have a debit balance include assets, expenses, and losses. Examples of these accounts are the cash, accounts receivable, prepaid expenses, fixed assets (asset) account, wages (expense) and loss on sale of assets (loss) account.

Cash on Hand is an asset account, and this means that debits increase its balance, and credits decrease that total. This account, therefore, is said to carry a debit (DR) balance.

Debits and credits are used in monitoring incoming and outgoing money in a business account. Simply put, debit is money that goes into an account, while credit is money that goes out of an account.

Debits and credits are accounting entries that record business transactions in two or more accounts using the double-entry accounting system. A very common misconception with debits and credits is thinking that they are “good” or “bad”. There is no good or bad when it comes to debits and credits.