Does a debit or credit increase inventory?

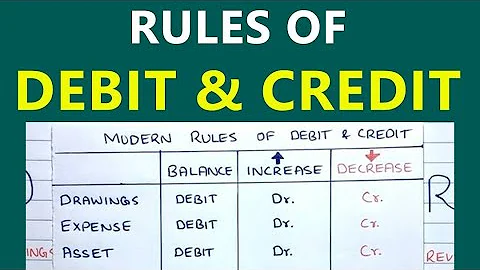

Merchandise inventory (also called Inventory) is a current asset with a normal debit balance meaning a debit will increase and a credit will decrease.

Inventory assets are recorded in your account ledger as debits when their value increases and entered as credits when their value declines.

The cost of products utilized from the stock on hand is calculated by subtracting closing stock from opening stock. To reflect how much stock is used for sales during the year, the opening stock is debited, and the ending stock is credited.

Debits increase asset accounts because they represent an infusion of value, whether it's cash received or inventory purchased. Credits decrease asset accounts, reflecting the outflow or consumption of resources.

Asset Accounts

In an accounting journal, increases in assets are recorded as debits. Decreases in assets are recorded as credits. Inventory is an asset account. It has increased so it's debited and cash decreased so it is credited.

To record the transaction, debit your Inventory account and credit your Cash account. Because they are both asset accounts, your Inventory account increases with the debit while your Cash account decreases with a credit.

Debit refers to an entry that increases assets or decreases liabilities. For example, when you purchase inventory with cash, you record a debit in your Inventory account because you are increasing your assets.

When an item is ready to be sold, it is transferred from finished goods inventory to sell as a product. You credit the finished goods inventory, and debit cost of goods sold. This action transfers the goods from inventory to expenses.

When making a journal entry, COGS should be debited and purchases and inventory accounts should be credited, showing the assets have been sold and their costs moved to COGS (one account is debited, and one or more other accounts are credited to balance the entry).

Inventory purchase journal entry

Say you purchase $1,000 worth of inventory on credit. Debit your Inventory account $1,000 to increase it. Then, credit your Accounts Payable account to show that you owe $1,000. Because your Cash account is also an asset, the credit decreases the account.

Is cogs a debit or credit?

You may be wondering, Is cost of goods sold a debit or credit? When adding a COGS journal entry, debit your COGS Expense account and credit your Purchases and Inventory accounts. Inventory is the difference between your COGS Expense and Purchases accounts.

When the company sells inventory to a customer on credit, it records a decrease in Inventory (credit) and an increase in Cost of Goods Sold (COGS) (debit), reflecting the cost of the inventory sold.

Debits increase asset and expense accounts while decreasing liability, revenue, and equity accounts. On the other hand, credits decrease asset and expense accounts while increasing liability, revenue, and equity accounts. In addition, debits are on the left side of a journal entry, and credits are on the right.

- First: Debit what comes in, Credit what goes out.

- Second: Debit all expenses and losses, Credit all incomes and gains.

- Third: Debit the receiver, Credit the giver.

Normally, the size of a company's inventory fluctuates with its sales. “It is expected that inventories will increase proportionately to increases in sales, but when sales decrease, inventories should also adjust downward,” adds Dany Couillard, Director, Business Restructuring, BDC.

The company would increase inventory by debiting inventory (increases inventory) and crediting cost of goods sold (reduces expense). If inventory per the physical count is less than what the system has recorded, then that means that more items were sold, and the company needs to increase cost of goods sold.

If the increase in inventory is due to returned merchandise, the balance sheet, income statement, and statement of stockholders' equity will be affected. The increase in the inventory account will increase assets while the increase in sales returns and allowances will decrease net sales on the income statement.

Inventory Credit means an immediately available credit issuable to Buyer to purchase from Seller inventory of the kind listed on Schedule 1.56 hereto or on Exhibit A of the Supply Agreement, or as otherwise provided on Schedule 2.9.

A debit of an expense on the income statement is an addition of that expense. It offsets the sales/revenue. In financial accounting it's an increase to cost of goods sold. You would debit it mainly when you are making a journal entry for selling inventory.

Debits increase the value of asset, expense and loss accounts. Credits increase the value of liability, equity, revenue and gain accounts.

What is the entry for inventory?

A journal entry for inventory is a record in your accounting ledger that helps you track your inventory transactions. Depending on the type of inventory and how much your business carries, there are different kinds of journal entries that may help you organize your financial expenses and earnings.

A credit to an asset account, like Merchandise Inventory, usually signifies a decrease in its value. If a company sells some of its inventory to customers, the Merchandise Inventory account would be credited, showing a decrease in assets.

Inventory becomes an expense when the product is sold. As soon as a customer gives you money in exchange for that item, it moves from the category of an “asset” to become an “expense” on your income statement.

What are the Golden Rules of Accounting? 1) Debit what comes in - credit what goes out. 2) Credit the giver and Debit the Receiver. 3) Credit all income and debit all expenses.

Answer and Explanation: The normal balance of the Merchandise Inventory account is a debit balance. Inventory represents the unsold stock that remains in the books and in the warehouse at the end of each accounting period.